1、作了一次营销活动,营销了1000人。事后统计结果,120人购买,其余人没有购买。请分别用矩估计法、极大似然估计法计算这个随机事件分布的参数(提示:该随机事件服从伯努利分布)

营销活动产生的购买的概率为:p = 120/1000

不会估计.....

2、推导线性回归参数估计得最小二乘、矩估计、极大似然估计,推导逻辑回归的极大似然估计公式。线性回归和逻辑回归的极大似然估计公式。

我能说我很懒么,不想打.....

线性回归和逻辑回归的极大似然法那个可以得到显性的公式解,哪个需要使用迭代法求解?

线性回归的极大似然法可以得到显性公式解,逻辑回归的极大似然需要使用迭代法求解。

解释极大似然法求解过程中用到的牛顿迭代法、随机梯度法的做法。

牛顿迭代法是一种在实数域和复数域上近似求解方程的方法。方法使用函数f(x)的泰勒级数的前几项来寻找方程f(x)=0的根。牛顿法最大的特点在于其收敛速度很快。

随机梯度法的优化思想是用当前位置的负梯度方向作为搜索方向,因为该方向为当前位置的最快下降方向,所以也称为是“最快下降法”。只有当目标函数为凸函数时,梯度下降法的解是全局解。一般情况下,其解不保证是全局最优解。

3、解释统计学算法中的超参的概念,请问目前统计方法中学习的线性回归、逻辑回归中涉及超参了吗?岭回归和Lasso算法中的超参分别是什么?超参的作用是什么?统计学习算法中如何确定最优超参的取值?

a、超参:是模型外部的配置,必须手动设置参数的值,不能从数据估计得到。

其主要特征有:1、模型超参数常用于估计模型参数过程中;2、模型超参数同程由实践者直接指定;3、模型超参数常根据给定的预测建模问题而调整。

b、如何确定最优超参数的取值,主要有两种方法:1、根据经验法则探寻其最优值;2、通过反复试验的方法。

c、线性回归与逻辑回归中没有涉及超参数。

d、岭回归与Lasso的超参数分别均为正则化项前面的系数。

e、超参数的主要作用一是通过调整超参数,可以找到使模型泛化能力的模型参数,即辅助估计模型参数;二是解决模型中有些不能直接从数据中估计得到问题。

4、比较统计分析法和统计学习(即机器学习)得到最优模型的思路。

统计分析在变量选择时主要是通过假设检验选取变量,而统计学习通过降维(主成分分析、因子分析)选取变量;

统计分析可直接通过散点图来验证模型假设,统计学习常作用于高维,不从直观观测;

统计分析通过多重共线性与强影响点来纠正模型,使模型更优,统计学习通过交叉验证来纠正模型。

5、二分类模型中(比如逻辑回归)的评估模型优劣的决策类和排序类评估指标分别包括哪些指标?

二分类模型(如逻辑回归)评估模型优劣的决策指标有:准确率、召回率、精确度、特异度等;

排序类评估指标主要有:ROC曲线(AUC)、K-S曲线(K-S统计量)、累计提升曲线(提升度)、Gini指数等;

# -*- coding: utf-8 -*-

"""

Created on Fri Jun 15 14:14:29 2018

@author: Rachel

"""

#%%

import pandas as pd

import os

from scipy import stats

import statsmodels.api as sm

import statsmodels.formula.api as smf

import numpy as np

import sklearn.metrics as metrics

import matplotlib.pyplot as plt

#%%

os.chdir(r"E:\Python_learning\data_science\task_0529\HW7")

tele = pd.read_csv('telecom_churn.csv')

#%%

#两变量分析:检验该用户通话时长是否呈现出上升态势(posTrend)对流失(churn) 是否有预测价值

cross_table = pd.crosstab(tele.posTrend, tele.churn, margins=True)

cross_table

#%%

def percConvert(ser):

return ser/float(ser[-1])

cross_table.apply(percConvert, axis=1)

#%%

print('''chisq = %6.4f

p-value = %6.4f

dof = %i

expected_freq = %s''' %stats.chi2_contingency(cross_table.iloc[:2, :2]))

#%%

tele.plot(x='posTrend', y='churn', kind='scatter')

#%%

train = tele.sample(frac=0.7, random_state=1234).copy()

test = tele[~ tele.index.isin(train.index)].copy()

print(' 训练集样本量: %i \n 测试集样本量: %i' %(len(train), len(test)))

#%%

#使用训练数据集建立在网时长对流失的逻辑回归

lg = smf.glm('churn ~ posTrend', data=train,

family=sm.families.Binomial(sm.families.links.logit)).fit()

lg.summary()

#%%

train['proba'] = lg.predict(train)

test['proba'] = lg.predict(test)

test['proba'].head(10)

#%%

test['prediction'] = (test['proba'] > 0.5).astype('int')

#%%

# 混淆矩阵

confusion_matrix = pd.crosstab(test.churn, test.prediction, margins=True)

#%%

# 计算准确率

acc = sum(test['prediction'] == test['churn']) /np.float(len(test))

print('The accurancy is %.2f' %acc)

#%%

# 计算召回率

recall = confusion_matrix.ix[0, 0] / confusion_matrix.ix[0, 'All']

print('The recall is %.2f' %recall)

#%%

#绘制ROC曲线

fpr_test, tpr_test, th_test = metrics.roc_curve(test.churn, test.proba)

fpr_train, tpr_train, th_train = metrics.roc_curve(train.churn, train.proba)

plt.figure(figsize=[3, 3])

plt.plot(fpr_test, tpr_test, 'b--')

plt.plot(fpr_train, tpr_train, '')

plt.title('ROC curve')

plt.show()

#%%

print('AUC = %.4f' %metrics.auc(fpr_test, tpr_test))

#%%

# 向前法

def forward_select(data, response):

remaining = set(data.columns)

remaining.remove(response)

selected = []

current_score, best_new_score = float('inf'), float('inf')

while remaining:

aic_with_candidates=[]

for candidate in remaining:

formula = "{} ~ {}".format(

response,' + '.join(selected + [candidate]))

aic = smf.glm(

formula=formula, data=data,

family=sm.families.Binomial(sm.families.links.logit)

).fit().aic

aic_with_candidates.append((aic, candidate))

aic_with_candidates.sort(reverse=True)

best_new_score, best_candidate=aic_with_candidates.pop()

if current_score > best_new_score:

remaining.remove(best_candidate)

selected.append(best_candidate)

current_score = best_new_score

print ('aic is {},continuing!'.format(current_score))

else:

print ('forward selection over!')

break

formula = "{} ~ {} ".format(response,' + '.join(selected))

print('final formula is {}'.format(formula))

model = smf.glm(

formula=formula, data=data,

family=sm.families.Binomial(sm.families.links.logit)

).fit()

return(model)

#%%

candidates = ['churn','subscriberID','AGE','incomeCode','duration','peakMinAv','peakMinDiff']

data_for_select = train[candidates]

lg_m1 = forward_select(data=data_for_select, response='churn')

lg_m1.summary()

#%%

#绘制ROC曲线

train['proba'] = lg_m1.predict(train)

test['proba'] = lg_m1.predict(test)

fpr_test, tpr_test, th_test = metrics.roc_curve(test.churn, test.proba)

fpr_train, tpr_train, th_train = metrics.roc_curve(train.churn, train.proba)

plt.figure(figsize=[3, 3])

plt.plot(fpr_test, tpr_test, 'b--')

plt.plot(fpr_train, tpr_train, '')

plt.title('ROC curve')

plt.show()

#%%

print('AUC = %.4f' %metrics.auc(fpr_test, tpr_test))

#%%

#模型的膨胀系数

def vif(df, col_i):

from statsmodels.formula.api import ols

cols = list(df.columns)

cols.remove(col_i)

cols_noti = cols

formula = col_i + '~' + '+'.join(cols_noti)

r2 = ols(formula, df).fit().rsquared

return 1. / (1. - r2)

# In[18]:

candidates = ['churn','subscriberID','AGE','incomeCode','duration','peakMinAv','peakMinDiff']

exog = train[candidates].drop(['churn'], axis=1)

for i in exog.columns:

print(i, '\t', vif(df=exog, col_i=i))

1、列联表

churn 0.0 1.0 All

posTrend

0.0 0.455745 0.544255 1.0

1.0 0.669100 0.330900 1.0

All 0.557031 0.442969 1.0

卡方检验

chisq = 158.4433

p-value = 0.0000

dof = 1

expected_freq = [[1013.24025411 805.75974589]

[ 915.75974589 728.24025411]]

从上结果看,该用户通话时长是否呈现出上升态势(posTrend)对流失(churn) 是有预测价值

2、混淆矩阵

prediction 0 1 All

churn

0.0 348 235 583

1.0 170 286 456

All 518 521 1039

准确率:The accurancy is 0.61召回率:The recall is 0.60

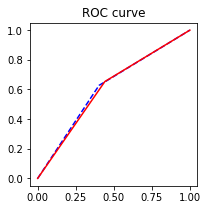

ROC曲线

AUC = 0.61213、逐步回归选择变量

<class 'statsmodels.iolib.summary.Summary'>

"""

Generalized Linear Model Regression Results

==============================================================================

Dep. Variable: churn No. Observations: 2424

Model: GLM Df Residuals: 2417

Model Family: Binomial Df Model: 6

Link Function: logit Scale: 1.0

Method: IRLS Log-Likelihood: -1012.7

Date: Fri, 15 Jun 2018 Deviance: 2025.4

Time: 17:51:02 Pearson chi2: 2.26e+03

No. Iterations: 7

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

Intercept 6.4997 2.136 3.043 0.002 2.314 10.686

duration -0.2382 0.011 -21.227 0.000 -0.260 -0.216

peakMinDiff -0.0029 0.000 -7.918 0.000 -0.004 -0.002

AGE -0.0195 0.004 -4.760 0.000 -0.028 -0.011

subscriberID -5.015e-08 2.84e-08 -1.765 0.078 -1.06e-07 5.54e-09

peakMinAv 0.0007 0.000 1.789 0.074 -6.88e-05 0.002

incomeCode 0.0054 0.003 1.660 0.097 -0.001 0.012

================================================================================

"""

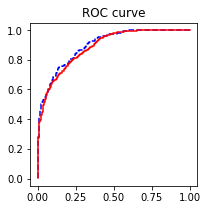

ROC曲线:

AUC = 0.8974

膨胀系数:

subscriberID 1.006376917076832

AGE 1.0539373172811175

incomeCode 1.0233464772559815

duration 1.0383978966834935

peakMinAv 1.0380990598521813

peakMinDiff 1.036565610813066